PSLF & a Prescription for the MOHELA Woes

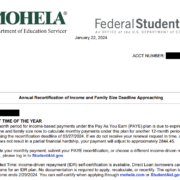

Starting May 1st, all records will no longer be available on MOHELA’s website and will move to studentaid.gov. To make sure that nothing is lost or omitted in the transition, keep copies of messages, letters, receipts, etc. for yourself.